But if you step back and look at a bigger view, you see another interpretation:

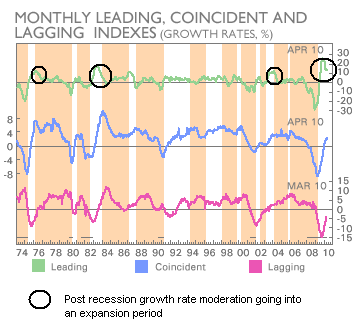

This multi-recession chart is also shown in the article (with the notes in black added) and shows a typical breaking of the "speed limit" coming out of a bad recession and then a moderation to a more steady speed going into the expansion cycle. The ominous 1 year dip would appear to be this moderation phase in the cycling.

You see something similar in the just released Journal of Commerce JOCSINDS indicator in the 1 year time frame. But if you click "chart the performance" for this recovery speed measure, and click on the 5 year view, you see pretty much the same moderation pattern as in the ECRI chart above.

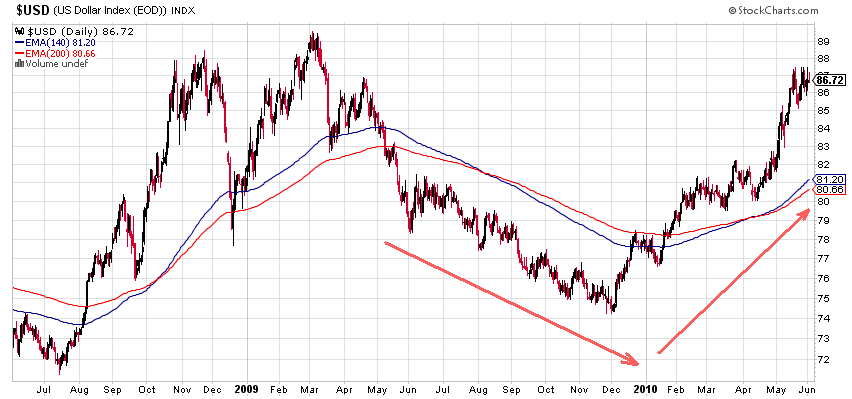

So why are commodities looking so bad? A moderating, stable recovery should be just fine for them. Well, you may not have to look any further than the US dollar chart to explain this. Commodities and the dollar are strongly correlated inversely. There has been something of an aberrant, monster rally in the USD in the face of the European debt turmoil. It's aberrant because the USD has all the same problems as the euro. What happens when the dollar rally fizzles? For now, the rally has correlated to a big dent in what would be a normal, strong recovery in commodities: (click on charts to enlarge)

Since the turn point at the start of the year, we've had a 17% rally in the USD and a 12% drop in the CRB. The two are not unrelated. Gold usually moves with commodities inverse to the dollar, but gold is climbing. And gold is coming to be viewed as an alternative currency. What's happening with commodities is mostly a currency thing, not an economic cycle thing. China's Shanghai index is in much the same predicament as the CRB. It has, to a large extent, been caught up in the slump of the euro because Europe is China's biggest export customer.

The currency thing is, of course, a debt thing; and that's a downer. So if you attach any predictive significance to current commodity performance, you would have to say it's forecasting debt domino problems, not problems from the normal economic cycles. The leading market groups such as the RLX, the Baltic Dry Shipping Index, the QQQQ, etc. all still seem to be positive. But the debt can they have successfully kicked down the road is another story and will continue to be a threat to derail all normal economic cycling until they pick up the can and fix it.

No comments:

Post a Comment