Well, if you believe, as I do, that our markets are being led by the big banks and their derivative troubles, especially in Europe, you better take a look at the following. Things are going from bad to worse with the banks. NIRP is crippling a beast already wounded by the quantum leap lower in commodity prices. An article at Seeking Alpha states "NIRP Is Absolutely Crushing Big Parts Of The Finance World".

Negative interest rates are the antidote to a normal, healthy free enterprise system. Banks are forced away from giving savers a return and making their money loaning to economic activity with a normal yield curve. What are they forced toward? They now have to devote their full attention to what Glass-Steagall bared them from doing after the banking fiasco of the 1930s, "investment banking", playing with commodity and all manner of toxic derivatives, which is what got us into this very mess to begin with! Yes, that's just what we need.

As I pointed out before back in October, the key outfit to watch for clues as to what might happen next is Deutsche Bank, the lead bank of Germany, the lead economy in all of Europe, the leader as we go into a socialist style banking takeover of our global economy. They have replaced the Swastika with the Derivative Pricing Model. Our entire free capitalist world is held captive to how these models play out, and, in particular, how they control our currencies.

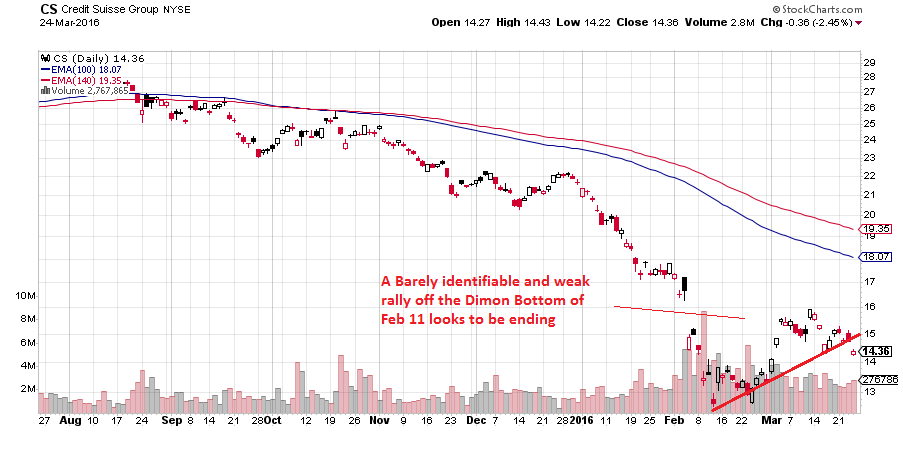

My fellow militant Austrian economist, Jeffrey Snider, just wrote an article at SA called "Credit Suisse And Deutsche Bank Still At The Forefront (Just Where They Don't Want To Be)". Here he quotes a mea culpa from Credit Suisse on their sipping of the Bernanke Kool-Aid with heavy bets on returning to normal economic growth in the Emerging Markets after the 2008 crisis. Tiajane Thiam, CEO of Credit Suisse, is giving a euphemistic review of Q4 that is paraphrased by Snider thusly:

In other words, the bank is admitting that it messed up in chasing high yield and EM credit and all the activities that surround them, vowing now to leave those areas as quickly as practical. It isn't so easy, though, as Thain's most recent ante in more lost investment banking jobs suggests."At the forefront" as Snider says, is indeed where DB is leading us ever onward: (click on images to enlarge)

Credit Suisse is also joined in that regard by the others that followed this policy success vision. Deutsche Bank, for example, was just put on negative ratings watch by Moody's. The ratings agency sees the same as Credit Suisse - that the strategy once followed and having been done leaves only further pain to undo it.

Make no mistake, we are getting into a market situation where the money flows of the big banks are taking over from GDP numbers, earnings, employment reports and the things that are supposed to operate markets. Many would argue that the aforementioned numbers have already been removed from the real economy anyway. But the derivative kingdom has staged a coup and is now calling the shots in the stock market, superseding economic numbers, real or fraudulent. This is a point Jeffrey Snider is making pretty clear in tracking the dollar shortage mess now getting to very dangerous levels. I wrote an article on this and its relation to gold and showed this amazing correlation Snider points out between the goings on at the big banks and our recent market selloffs:

The repo chart Snider shows has the dollar shortage recently doing a moon shot to the highest level since Lehman, 2008. The sloshing around of currencies at the big banks seems to be controlling the value of your favorite stock more than the employment report or about anything else these days. The out-of-control complexity of our credit based currencies and derivative linkages is what mostly matters anymore. The dollar shortage is beginning to seriously disrupt business in many countries, mainly the heavy commodity exporters, as this CNBC piece details. The list of such dollar shortage crises is growing.

The causes for this mushrooming menace in the currency markets are many, complex, convoluted, not understood well or reported by many. And I certainly don't understand all the mechanisms involved. But allow me, as someone who is viewing the forest, not the trees, to make an observation.

Our "money" over the last few decades has become purely a complicated series of credit transactions among banks, not based nowadays on much else besides creditworthiness. As JP Morgan is famous for saying, back in the sensible days of sound currency, "Gold is money. Everything else is credit". Thus the Moody's talk of downgrades for Deutsche Bank and the like is naturally having a jarring effect in the credit-crazed currency markets. The $700 trillion derivatives "bomb" that was partially detonated in 2008 may see more fireworks in this latest counterparty risk obsession in currencies.

Deutsche Bank, our fearless leader in the technical condition of the stock market, is also the world leader in derivatives.

Nearly a hundred years ago, after many years of looking the other way with the creeping policy of appeasement, it took a horrendous world war to stamp out the socialist rats enslaving the German people. Now, a computer algorithm version is taking over our growing taxes, the bills in our wallet, and our right to a growing economy. As I showed in Gold And Derivatives these Gestapo goons are even in the process of laying claim to your bank account to pay for their derivative indiscretions in the future.

In 1943, the Nazis were winning the war. After Pearl Harbor, Japan ruled the Pacific and we were bracing for an invasion at California. Hitler had drawn up the recently discovered construction plans for death camp locations in a divided America, the west half governed by Japan and the east half, with all the Jews, governed by Hitler. IBM was developing the first computer that would be used by the Navy to calculate its gunnery. Without the undivided focus and outrage of the world in the war effort, with every company making war parts and nearly every mom helping while her man was away fighting, the tide may not have been turned in 1943. Now, our global socialists with reckless derivatives as their main weapon are looking to enslave, not just the German people, but anyone who must pay taxes and has a bank account connected to a computer. They are farther ahead than the Nazis were in 1943, only with the world fast asleep. What's it going to take this time to stamp out these cyber socialists?

Let's all hope the all-knowing, super-hero Derivative Pricing Model continues to solve all our problems for us. It has gotten us this far.

No comments:

Post a Comment