When the earthquake hit in Washington last November, sliding everything to a more business friendly world, copper went on a Trump tear along with several other things. Does this have any staying power? Is there something in the world's wiring to back it up?

Jesse Moore has an excellent series of reports on copper at Seeking Alpha. He began predicting a bear-to-bull turn in copper back in March, 2016, when copper was in everyone's doghouse, including mine. He was saying that within 12-24 months the bear would be a bull. We are now 12 months from his call, and copper is stirring from its bear slumber. His first in the series was a country-by-country look at copper mining projects, and he compares his result with that of Chili's government. Why should we care about Chili's copper work? Because they are the biggest copper supply in the world, giving us about one third of the metal. The whole Chilean economy centers on copper. Then there is the International Copper Study Group (ICSG) that does a projection as well. Moore's summary:

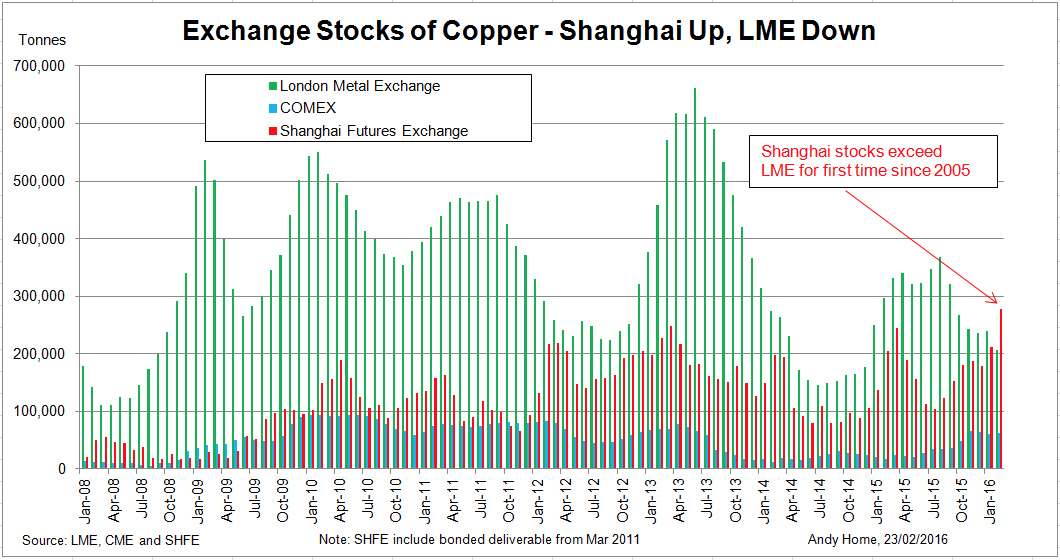

I believe both groups have not taken proper account for delays in a startup or ramp of new mines, grade reductions in Chile, water shortages leading to unplanned shutdowns, reduced capital expenditure, and the replacement of risk taking CEOs with risk averse CEO's who have slashed budgets across the world. Copper is not iron ore, and it is not nearly as easy to find and produce. The current copper price does not support growing supplies, and it appears that some producers have begun to put their collective shovels down ... In reality, the world needs another mega-project before 2020, and we just don't have one coming. The major deposits are, for the most part, found. $3.00 will easily bring on plenty of supply, but again, my belief is it will be too late. My guess is that we start to see the shortage become obvious near the end of the first half of 2017, prices will overshoot and what we saw during the China boom won't be out of the question"The China boom" he is talking about is what happened back in 2004, when China went ballistic building the future China - and over did it. China has been notorious for commodity hoarding to insure supply for their plans. And they did this with copper in 2004, when their Shanghai inventories did a rare thing. They rose above the LME (London Metal Exchange) inventories, the world's standard for metal storage, just in front of the crazy copper bull market that ensued back then. Moore shows on a chart that this rare occurrence has just now happened again, the first time since 2004.

Don't Ignore China

We need to pay attention to China and Asian copper usage in general because it accounts for about 62% of total copper usage, the Americas just 14% according to the ICSG pie chart shown in Moore's article treating copper demand. So forget Trump's building ambitions, copper began its breakout before the election. We need to know what's up in China.

China's construction contracts have continued a high rate of growth despite their economic slump, as have car sales. A lot of China's recent copper interest may lie in the aluminum vs copper wiring battle. They have been using a lot of the aluminum wire, because it is a very abundant metal with stable pricing running a fraction of that for copper. But aluminum wire has its problems. It must be alloyed to make it strong enough for wiring and this makes it less conductive. Copper can be used in a more pure form, especially pure, newly mined copper as opposed to the 50% of annual copper usage that is recycled. Only about 8% of scrap is made into wiring. So copper wire places nearly all its demand on the newly mined half of supply. Aluminum is also is subject to corrosion from moisture and other things and must be replaced much more often than copper. China is considering going to all copper for its wires, and this Moore says, will make a big, abrupt difference in copper demand:

Nearly half of all China's copper consumption goes towards grid infrastructure, and China has recently been discussing abandoning aluminum wiring in favor of more expensive, but reliable, copper wire. The outcome of which could drastically effect the demand for copper over the short termAltogether, 75% of global copper demand is for electrical wires. But a big problem with copper wire is price instability. This may explain a good bit of the stockpiling going on now in China.

Copper's Supply

On the supply side, copper mining has been suffering a pronounced decline in ore grades. In "Copper: A Bullish Decade Is Coming" Moore shows a graph for global mining revealing that copper content of ore coming out of the ground is half of what it was in 2008. The best fruit has been picked, and, unlike oil, there is no big shale bump to come to the rescue. Shale, as I have written about in other articles, is keeping oil prices moderate for at least a couple of years.

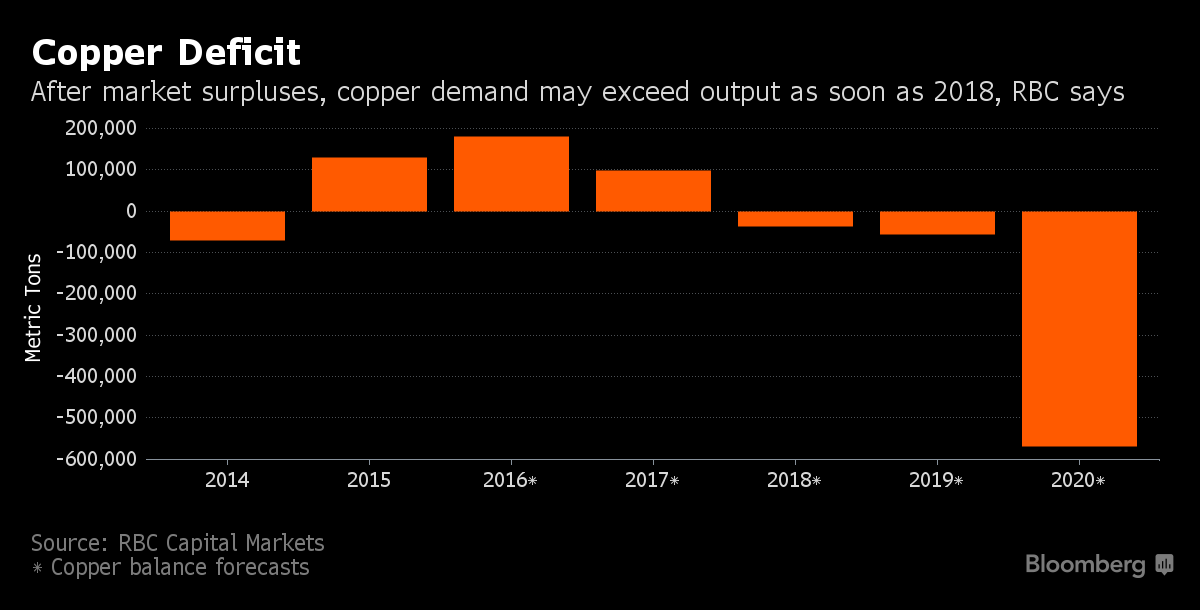

If nothing suddenly shows up like a copper shale, the projected departure of demand curve from supply curve is slated to transpire around 2019 according to mining.com and their infographic tour of copper. For 50 years, they've known about shale and the other "dreg oil" (bottom of the barrel) that would be flooded onto the market by a quantum leap to higher prices. There is no such thing for copper - just a continuous slide to more and more expensive grades of normal ore. The current labor problems of Escondida, the world's biggest copper mine and other disruptions may be bringing a looming copper deficit closer at hand. Mining.com isn't the only one projecting this timeframe. Moore includes an RBC Capital Markets chart saying the same thing.

These could be some of the reasons for "Doctor Copper Hiding in Shanghai Warehouse" as a Wall Street Journal online piece from about a year ago proclaimed, saying that, "the pickup in the price of copper isn't driven by a stronger Chinese economy." You could argue that all the price surge is from Chinese stockpiling and thus it will simply reverse when they figure they have enough. But as Jesse Moore points out, they did this same stockpiling thing in 2004, to the same level relative to the LME, after which copper did a huge climb. China probably knows the copper market better than about anyone, being much more dependent on it than any country. They seem to know that they will have to buy higher later.

So are we running out of copper? No we are not. In fact we have mined way less than half of what's in the ground and almost all of that is still in circulation! Roughly half of copper usage is recycled metal. Even for silver, the recycled portion of demand is just about one fourth. Copper is by far the most reused resource on the earth. We don't burn it up like oil. It's relatively rare and doesn't rust into oblivion like iron. It only takes 15% of the energy to recycle copper as it does to mine it. How much gets recycled and refined is a function of the copper price. How much of the low grade, expensive ore that gets dug out is also a function of the copper price. We should perhaps draw a distinction here between peak oil and peak copper. We are enjoying a reprieve from peak normal oil with shale, tar sands, and so on. This could be for years, but there isn't that much of it to be exploited compared to the normal copper that's left to be recycled and still in the ground. We are not running out of copper.

We Are Running Out Of Cheap Copper

The looming supply deficit being projected is all a matter of copper pricing. It will be about market pricing and what that will be bringing to the plate. And it will be about any sudden changes to copper demand, like a China switch away from the aluminum electrical wiring. Added mine capacity doesn't come quick or cheap. And 92% of new copper wire must be pure, newly mined copper.

This aluminum/copper wire problem in China is being further aggravated by the massive internet speed bottle neck going on now in our last mile networking. I discuss this in detail in my article "The Impending Super-Cycle In The All Glass Internet" noting that as China struggles to become a superpower, their internet speed ranks #82 in the world. As all new buildings everywhere are becoming very populated with our new web connected devices, wiring material is being pushed beyond its limits now.

The disruptive switch-over from copper hybrids to an all fiber last-mile in urban areas means a very expensive mess. So ever increasing speeds have dictated a next generation of DSL on the very old copper that's already there. This new standard known as G.fast is being deployed. It is a nice speed improvement, and often compared to broadband fiber based on lab results, but will suffer the usual shortcomings of anything imposed on copper. The fade with distance is very bad relative to fiber. Also, there is a vast difference in the normal existing copper and what they are using in the lab for these tests. I refer you to Jim Wegat for this. He was an optics engineer for Terabeam, and when I asked him about this supposed equality of G.fast copper to fiber, he said it:

... is confusing the wiring in homes and neighborhoods with the high quality wire used in the study by Alcatel-Lucent. It is a bit like saying that a specially designed car broke the land speed record and since most Americans have cars they should be able to break the land speed record with their cars too.

If we are needing this super pure, pristine copper to handle our new last mile, the cruddy, slow aluminum is out of the question. No wonder they are wanting to tear out the aluminum.

Fiber vs Copper

If I were vice president in charge of China's building programs, I would just cut to the chase and future proof my structures with all fiber and not even mess with copper. But I suppose when you must deal with a complicated budgetary mess and calendar of progress that dictate less than ideal science, it's not as simple as that.

There is a lot of debate on the pros and cons of fiber vs copper for LAN and building cables. Copper cabling suffers from electromagnetic interference between cables, fiber is immune to electric or magnetic interference. Copper is subject to disruption from lightening and water. Fiber is immune to that. I am not an expert on all this. I will just offer what Commscope has to say per a write-up titled "Will Fiber Ever Replace Copper Cable" on their website concerning what's happening in China.

Data centers in China are averaging 40% fiber and 60% copper while the very large data centers are about 70% fiber. But with "intelligent buildings" copper still dominates in-building networks:

"This is mainly due to the high cost of fiber-to-the-desk (FTTD) system as well as fiber’s high requirements for application environment and routine maintenance. Therefore, in the market of intelligent buildings, the percentage of fiber usage is only around 30 percent, while copper cabling occupies the remaining 70 percent market share. "

The Chinese seem to be very cost sensitive, having put in a lot of the aluminum wire, and now are averse to the high cost of FTTD. And that 70% copper market share may be looking better because of a new technology they are developing called Power over Ethernet (PoE):

"...when it comes to the intelligent buildings market, copper cable is facing new opportunities brought on by the fast landing of the Power over Ethernet (PoE) application"The extraordinary copper stockpiling pointed out by Moore that took place in 2005 and just recently in 2015 was done with little fan fare or publicity, as important as it is to investors. But in a Reuters report from 2015, cited in Moore's part two article on copper (demand) China's government gives us a glimpse of their plans for copper. China does things by five year plans, and this report covers the 2015-2020 plan with the title "UPDATE 1 - China Targets $300 bln Power Grid Spend Over 2015-2020 - Report" and cites government sources in China. That's a third of a $trillion spent on wires, a big number, but to put the numbers in perspective, the plan calls for installing transmission line length over 2015-2020 equal to more than twice the 2014 level. That's over twice the cable strung in five years than was strung in the previous one hundred. The report, in what would seem to be an understatement, said all this is “likely to provide a boost for sectors like copper.” And it also makes pretty clear the choice in the aluminum vs copper battle:

“The plan was aimed at increasing the reliability of power transmission, which would favour copper-based cables over cheaper alternative aluminium-based cables, said Yang Changhua, senior analyst at state-backed research firm Antaike.”If you look at a historical chart of China's copper imports, as in this report, you see an interesting connection to these five year plans. Over the 5 year plan 2000-2005, copper importing was flattish going from 70 to 50 (10 thousand tons). Then after the unusual stockpiling blitz by China in 2005, when the Shanghai inventories exceeded the LME the first time, the 2005-2010 five year plan saw copper imports do a massive climb from 50 to 300. This was accompanied by a strong climb in copper from $1.43 to $4.27. In the five years since, the imports have again been flat, going from 300 to 300, with the price of copper drifting back down. In fact, if you overlay this China copper import chart with the copper price chart, you get a remarkable correlation except briefly for the 2008 financial crisis. Now, the Shanghai inventories have exceeded LME once again, and you have to wonder what's up with China's plans. Keep in mind that they probably know the copper market better than anyone.

So a big new wave of demand could be coming for newly mined wire grade copper. The supply projections above may have a tough time keeping up with it.

The supply would have to be accomplished with higher prices. A lot of what's going on in China probably applies to other emerging Asian countries, and that block is 62% of copper's demand. China apparently sees this as a big enough problem to justify a whole new round of stockpiling.

Another consideration with copper supply is its relation to gold. Copper is usually found wherever gold has formed, and you can't read much geology on miners without seeing "gold-copper, copper-gold" and similar terminology. The basic fact is that much copper is mined as a co-product or by-product with the vastly more lucrative gold content. If the price of gold is cutting production, a copper shortage has to run a ways before operations are being ramped up just for the copper. Thus you have to be mindful of the relative status of gold and copper bulls and bears. Right now we have gold looking bearish since late last year while a copper bull may be on its way. Almost always in history, gold and copper bulls have run in tandem. If now they are to run in opposite directions, it would be an oddity. Technically, gold is in limbo now between long-term bull and possible new bear in the $1250 area. So this bears watching. We will probably have a copper shortage if gold continues its long-term bull market, but if gold continues its retreat from last year, the copper shortage could become severe.

{kind=link}

{kind=link}

No comments:

Post a Comment