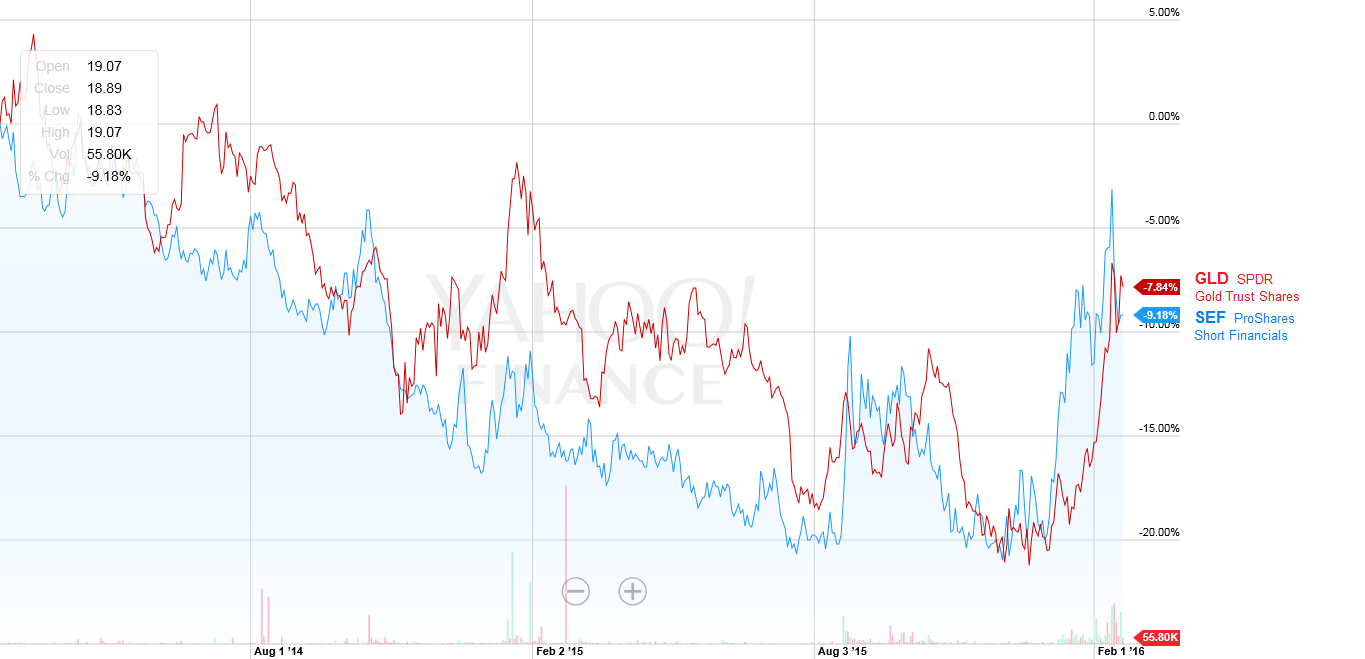

In horseshoes, we call this a "leaner," the next best thing to a dead ringer. Here we see that gold has been strongly correlating to the inverse of the financials. It's the banks that gold seems to be mainly concerned with ...Over the years, there has been a very strong correlation between the big gold moves and bank health. This isn't talked or written about very much as gold is supposed to move opposite the dollar, opposite the stock market, or as a result of interest rate changes. But if you examine history, you find that the most massive gains in the gold miners tend to happen when very serious trouble is engulfing the banking world.

It certainly was so in the 1930s. As I pointed out in my article "A Study In Crashology", there were a lot of moving parts in the puzzle back then. Most people think the stock market crash in 1929 was the immediate cause of the Depression. But this market event was just a big valuation correction of speculation in the Roaring '20s, and just a garden variety recession was going on in the economy. In fact, we were recovering from this recession when the real trouble started. What happened to cause something more was the involvement of the banks with Wall Street in all this reckless speculation, and the fact that many banks lost so big in the stock crash. This giant problem led to the Glass-Steagall Act of 1934 that put up a wall between banks and investment - no mingling of depositors' money and speculation. More than any other factor, this banking illness induced one of the mega bull markets in gold mining. In historical context, it looks like this:

Another bout of serious banking problems hit during the Savings and Loan Crisis of the 1980s. Before this was over, nearly 1 out of 3 Savings and Loans went under at a horrendous bail-out cost. Despite all the supposed protections built into the system, this speculation mess cost every tax paying American over $1000 chipped in from their own wallets. This was during a grinding bear market in gold after the 1980 bull market peak, but the gold miners did a spectacular climb at the peak of the bank failures:

There was the stock market crash of October, 1987, but the gold miners got clobbered along with that, and the only other significant thing going on in that year to cause a whopping 100% gain in the XAU miner index in a gold bear market in less than a year was the severe trouble in the banking world.

At the Federal Reserve History web site, the piece "The Banking Panics of 1931-1933" blatantly said that gold responded to the banks:

On September 21, 1931, Great Britain left the gold standard—that is, withdrew its promise to provide a specific amount of gold in exchange for its bank notes (Wicker 1996). Foreigners became concerned the United States would do the same and began converting their dollar assets to gold. This external drain caused a large reduction in the US gold supply. At the same time, depositors became concerned about the safety of banks and withdrew currency from their accounts, creating an internal drain on the banking system (Friedman and Schwartz 1963). Together, these external and internal drains reduced the money supply, deepening the deflation which propagated the depression.

Can such a horrible thing happen again? Don't we have the FDIC to protect us? If a mass withdrawal panic were to happen again, the FDIC would cover about the first 1% of failure. At the leading edge of negative interest and the other bank destroying avant-garde measures is Japan, and there we see home safe sales are soaring. This is not a good pied piper to be following.

You may have noticed on the above chart of bank failures that a boiling pot of trouble comes along every 36 years, but at the 1944 juncture, just the opposite happened - a virtual disappearance of bank trouble - for 36 years. What strange thing happened here, and what does it have to do with gold? Bretton Woods happened and it had everything in the world to do with gold.

This was a conference in July, 1944 in Bretton Woods, New Hampshire, where 730 delegates from over 40 nations came together because they were all sick of the banking and currency troubles that had beset the nations ever since we strayed from monetary gold and silver starting in the late 1800s. We created the Federal Reserve System in 1913 thinking we had little need for precious metals in our modern economies. And we had experienced a world war and a punitive treaty against Germany that resulted in an inflationary destruction of that nation. This had led to yet another world war. And in the meantime, we had allowed wanton speculation in the bank world to take depositors' life savings and demean our whole economy into an unnecessary depression.

We fixed all that. Glass-Steagall was put into effect in the mid '30s to protect our banks from the careless speculators, and Bretton Woods was signed in 1944 to strictly tie the world's finances again to gold. The goal was to prevent competitive currency devaluations and over leveraged Wall Street (vs real economy) investing. Does this sound familiar ? By Wikipedia's account,

In the 1920s, international flows of speculative financial capital increased, leading to extremes in balance of payments situations ... Flows of speculative international finance were curtailed [ by Bretton Woods ] by shunting them through and limiting them via central banks. This meant that international flows of investment went into foreign direct investment (FDI) - i.e., construction of factories overseas, rather than international currency manipulation or bond marketsThis sounds like all the things that need to be stopped today. At Bretton Woods, the upshot of their wrangling was that the US dollar was strictly set to convertibility to gold, and the rest of the world's currencies strictly (+ or - 1%) set to the US dollar. Could such a thing even really work? Well, judge for yourself:

A negative balance of payments, growing public debt incurred by the Vietnam War and Great Society programs, and monetary inflation by the Federal Reserve caused the dollar to become increasingly overvalued. The drain on US gold reserves culminated with the London Gold Pool collapse in March 1968. By 1970, the U.S. had seen its gold coverage deteriorate from 55% to 22%. This, in the view of neoclassical economists, represented the point where holders of the dollar had lost faith in the ability of the U.S. to cut budget and trade deficits.Then, president Clinton undid the Glass-Steagall part. And we have had one banking crisis after another ever since with the biggest one probably yet to come.

In 1971 more and more dollars were being printed in Washington, then being pumped overseas, to pay for government expenditure on the military and social programs ... In response, on 15 August 1971, Nixon ..."closed the gold window", making the dollar inconvertible to gold directly, except on the open market. Unusually, this decision was made without consulting members of the international monetary system or even his own State Department, and was soon dubbed the Nixon Shock.

Regarding the historic panorama of bank failures shown above, you may notice that the great gold bull market of the 1970s had no correlating bulge of bank failures. We can actually explain that in just three words - Richard Mischievous Nixon. He said he wasn't a crook, but his Watergate lying was just the tip of the ethics iceberg. He passed himself off in elections as a fiscal conservative, but per the account at Investopia "The Great Inflation of The 1970s":

Nixon ran budget deficits, supported an incomes policy and eventually announced that he was a Keynesian ... John Maynard Keynes was an influential British economist of the 1930s and 1940s. He had advocated revolutionary measures: governments should use countercyclical policies in hard times, running deficits in recessions and depressions. Before Keynes, governments in bad times had generally balanced budgets and waited for malinvestments to liquidate, allowing market forces to bring a recovery.

"Malinvestment" is the key word David Stockman now uses in describing the unprecedented problems banks face today, where natural market forces have been obliterated. Stockman was Reagan's Office of Management and Budget (OMB) chief and wrote the recent best seller "The Great Deformation" describing this historic destruction of free market forces. He greatly helped us get out of Nixon's '70s mess. Going into the 1972 election, Nixon wanted cheap money no matter what:

President Nixon's primary concern was not dollar holders or deficits or even inflation ... Nixon fired Fed Chairman ... Martin, and installed presidential counselor Arthur Burns as Martin's successor in early 1971. Although the Fed is supposed to be solely dedicated to money creation policies that promote growth without excessive inflation, Burns was quickly taught the political facts of life. Nixon wanted cheap money: low interest rates that would promote growth in the short term and make the economy seem strong as voters were casting ballots.Nixon got his cheap money and the election. He said "We'll take inflation if necessary, but we can't take unemployment". We soon had both after he was bounced out of office. Jeremy Sigel (Stocks For The Long Run author) is quoted as rating this "the greatest failure of American macroeconomic policy" since the Depression. And although Americans generally think of this dark period as the fault of the OPEC oil shocks, The Wall Street Journal is quoted as saying, "OPEC got all the credit for what the U.S. had mainly done to itself."

So the 1970s saw a great gold bull market, no bulge of bank failures, but all the key things that cause bank failures, dished out by Nixon, were there. The gold market knew this. The banks, however had just been through the massive strengthening measures of nearly 30 years of Bretton Woods and had withstood the relatively brief onslaught by Nixon after he did the hatchet job on the agreement in 1971. Thus, no bank failure bulge on the map above. We are in a far, far different situation today with our banks.

Actually, the actions of Nixon did have their ultimate impact on banking, for it was the destabilized interest rates he caused that were a prime cause of the Savings and Loan Crisis. It just took about 10 years to boil up.

So will we have a return of the 36 year cycle of banking trouble start to boil again in 2016, 36 years after 1980 and the start of the last banking failure debacle? We have been papering over banking problems since 2008 with an unprecedented blizzard of measures unhinged from gold. The gold miners have certainly looked at the bank world this year and clearly do not like what they see there. As seen above, their market signal has been reliable in the past. It isn't really a secret that bad energy company loans issued in the aberrant zero interest frenzy of the last several years are a problem right now for banking. And many are saying it's just a passing energy sector thing, contained, like sub-prime was to be. But if you dare to peak at a broader picture of this bad loan thing, you see this:

But as I said in my recent article on Jim Grant's helicopter money call and its relation to gold:

The printing presses can seemingly fix anything forever, but the ultimate in all this may be evident at what Jim Grant referred to above as the leading edge of all this monetary lunacy, Japan. There we see home safe sales are skyrocketing. And in another avant-garde corner, we have a recent piece on Italy's banks and who and how to bail them out of their mismanagement and insolvency. After exploring all the "emergency liquidity" options, the article concluded:Gold and bank troubles are strongly linked, and both appear poised for bull markets.

The real threat is if the local population wakes up to the risk of holding their savings in a financial system that is now teetering on the edge, something Renzi [ Italy's prime minister ] himself admitted when he said that he "hoped to use a liquidity backstop to contain investor panic, which could result in a run on deposits and affect banks’ liquidity." Because even if it buys up every bond, loan and stock in the world, the ECB will not be able to fix the public's loss of trust in fractional reserve banking.

No comments:

Post a Comment