Sunday, September 19, 2010

Cancel Breakout Alert

Continental Minerals is being acquired by Jinchuan Group it was announced Friday. There shouldn't be much more rise in the stock as it is near the present buyout price (I hadn't seen the announcement yet on Friday when I did the previous post). An agreement has been signed, it looks like a done deal.

Wednesday, September 15, 2010

Breakout Alert

Continental Minerals (KMKCF) is a junior Canadian gold/copper/silver miner that mines in China. From what I read, they have a promising property there with well over 4 million oz. of gold and 11 million oz. of silver. The stock seems to be doing a promising breakout (click to enlarge):

Since the big gold rally late last year, in which KMKCF participated nicely, the stock has been idling in a megaphone formation. After a false breakout in April to about $2.50, it may have completed this formation today with a real breakout with some building volume. I like the moving average geometry and the heavy 24% insider interest. If it doesn't do a breakout now, it probably will soon if gold keeps working its way higher.

Since the big gold rally late last year, in which KMKCF participated nicely, the stock has been idling in a megaphone formation. After a false breakout in April to about $2.50, it may have completed this formation today with a real breakout with some building volume. I like the moving average geometry and the heavy 24% insider interest. If it doesn't do a breakout now, it probably will soon if gold keeps working its way higher.

Sunday, September 12, 2010

Quantifying The Insider Edge

As a follow-on to the importance of insider ownership level in considering gold stocks discussed in my previous post, I'll present a little number crunching here. I looked at a bigger sample size of gold stocks than just the 10 listed before with their big out-performance of the HUI to get a better handle on the relation, if any, between insider ownership level, size of company, and stock performance. I tossed out the ultra-microcaps less than $50 million or trading for less than 50 cents. I also tossed out the slower moving majors, with insider percentages typically not much effected by insider buying. I took a sampling of 51 such gold mining stocks from my gold list that trade on US exchanges with SEC standards of reporting. I sliced and diced this group into 3 market cap sizes and plotted their 1 year stock performance vs level of insider interest. Here is the result:

There is much less sensitivity to company size than I was expecting to find. The middleweights move about as fast as the featherweights. There is also little sensitivity to price range. I was expecting to find that as you go down the price range, the heavily insider owned stocks would curve sharply up in gain - down to the trash threshold, which is around $2 for stocks in general, but seems to be more around $1 for gold stocks. When I did a cluster chart for this, however, I got essentially random clutter.

The one big sensitivity that reaches off the page and slaps me in the face is what happens as you go below 2% insider interest level - a huge booby trap for performance. The individual stock performances vary widely, but this is an extremely poor averaging group - to be avoided like the plague. The large size group doesn't fall off as bad as the other two, but their size could be masking decent insider interest in many cases without having the needle moved much in percent. But the smaller companies, where any serious insider interest moves the needle off zero, are poison at these small numbers.

I have three chronic pains in my gold stock line-up in my fund, I call them the three stooges, and when I checked what their number was, sure enough all three stooges were toting less than 2%. That may be the last straw for them.

There is much less sensitivity to company size than I was expecting to find. The middleweights move about as fast as the featherweights. There is also little sensitivity to price range. I was expecting to find that as you go down the price range, the heavily insider owned stocks would curve sharply up in gain - down to the trash threshold, which is around $2 for stocks in general, but seems to be more around $1 for gold stocks. When I did a cluster chart for this, however, I got essentially random clutter.

The one big sensitivity that reaches off the page and slaps me in the face is what happens as you go below 2% insider interest level - a huge booby trap for performance. The individual stock performances vary widely, but this is an extremely poor averaging group - to be avoided like the plague. The large size group doesn't fall off as bad as the other two, but their size could be masking decent insider interest in many cases without having the needle moved much in percent. But the smaller companies, where any serious insider interest moves the needle off zero, are poison at these small numbers.

I have three chronic pains in my gold stock line-up in my fund, I call them the three stooges, and when I checked what their number was, sure enough all three stooges were toting less than 2%. That may be the last straw for them.

Sunday, September 5, 2010

The Problem With Gold Stocks

I like to analyze stocks by looking at a company's long-term financial results - cash flow, revenue, and what not, and looking at the interplay of these things with stock price. But I have found this approach to be all but useless in picking gold stocks. The performance of gold miners has nothing to do with their current financials other than simply having enough capital to pursue their projects. You see valuation ratios all over the map during their big climbs, much more so than with any other type of stock. They defy about any monetary type of analysis that may work reasonably well on stocks in general.

So how do you analyze the miners other than projecting the price of gold? Well, you have to resort to leaning on the expert opinion from the people who know more about gold mining than you ever will. These people can be book writers, commentators, newsletter writers, or Ralph, your barber. But all these people suffer from one or both of two key shortcomings (1) they are not geologists and (2) they are not officers of the mining company. It stands to reason that these are the people who know at least as much as the most informed newsletter writer, and probably more. I wouldn't think the company's officers surrender all the key information they possess to anyone on the outside.

So how does the average Joe Investor glean guidance from these people in the know ? First, you can get a feel for how good a management is by just looking at their stock performance over the course of the gold bull market so far. If the stock persistently shows little correlation to a rising gold price over the years, you have to wonder about the market's judgment on the management's ability. If the stock is to take advantage of a future rise in gold's price, it means this company's leaders are going to have to suddenly find a lot of new gold or change their management stripes. The odds are against both. I ran across a thoughtful piece in the archives at kitco.com "Industry Overview: Gold Mining & Exploration" by Derrick Irwin CFA that discusses this dilemma of gold stock analysis. His take:

How is this strong insider interest line up playing out over the past year ? Well, if you take the top 10, leaving off the low 11% of Midway, a lot of which is recent buying; and figure this portfolio's performance, you get +65% vs about +19% for the HUI gold stock index since this time last year.

The problem with gold stocks is you can't depend on our trusty valuation ratios, cash flow curves, or other normally useful parameters. Gold stock value is not about money put on past statements, its all about pulling future ore from their properties. You have to analyze the price of gold with all its complexity and danger. But most importantly, you must look inside the minds of the people who run the companies.

So how do you analyze the miners other than projecting the price of gold? Well, you have to resort to leaning on the expert opinion from the people who know more about gold mining than you ever will. These people can be book writers, commentators, newsletter writers, or Ralph, your barber. But all these people suffer from one or both of two key shortcomings (1) they are not geologists and (2) they are not officers of the mining company. It stands to reason that these are the people who know at least as much as the most informed newsletter writer, and probably more. I wouldn't think the company's officers surrender all the key information they possess to anyone on the outside.

So how does the average Joe Investor glean guidance from these people in the know ? First, you can get a feel for how good a management is by just looking at their stock performance over the course of the gold bull market so far. If the stock persistently shows little correlation to a rising gold price over the years, you have to wonder about the market's judgment on the management's ability. If the stock is to take advantage of a future rise in gold's price, it means this company's leaders are going to have to suddenly find a lot of new gold or change their management stripes. The odds are against both. I ran across a thoughtful piece in the archives at kitco.com "Industry Overview: Gold Mining & Exploration" by Derrick Irwin CFA that discusses this dilemma of gold stock analysis. His take:

We believe the most important factor to consider when evaluating an exploration company is the quality of management. In analyzing mining companies, we evaluate managements' experience in the exploration industry, and their track record for discovering gold deposits in the past. This is particularly relevant in regards to the geology team members, who will need to make important decisions regarding where to look for gold anomalies and how to proceed with drilling. On the management side, can the team attract continued investment to fund ongoing exploration activities?But there is perhaps a more direct way of tapping the knowledge and confidence of the management of a public mining company - insider buying and ownership level. They are putting their money where their knowledge is when they make these publicly available transactions. When these people place their personal money with an individual company in an arena where individual stock performance is very shaky, it means something. Irwin's opinion:

In our view, significant insider ownership is one of the most promising indicators of a healthy exploration company. Management is close to the exploration process and clearly understands how encouraging exploration results actually are, or what the status of agreements with vendors and development partners actually is. We also view management participation in follow-on offerings as a sign of continued faith in the prospects of an exploration company. We do not look at a "threshold" level of management ownership, but we do place higher value on larger ownership percentages. Also, we look for depth of ownership among management - does the whole board and management team hold significant shares, or are the shares concentrated in the hands of a founder or one large owner? A strong board and management team with significant share ownership is one of the most positive signs that an exploration company is healthy, in our view.With that in mind, I surveyed the miners that report insider activity (in the US anyway) and found some that currently have unusually high levels of insider held shares. Here is the top tier:

AZC Augusta Resource Corp 20%Midway Gold is the laggard of this group with 11%, but a whopping 64% of that insider ownership level has come about just over the last two years - a lot of recent insider buying.

NSU Nevsun Resources Ltd. 20%

XPL Solitario Exploration & Royalty Corp 15%

MDW Midway Gold Corp 11%

TLR Timberline Resources Corp 22%

PZG Paramount Gold & Silver Corp 34%

UXG US Gold 25%

GORO Gold Resource Corp 49%

NG NovaGold Resources Inc 32%

ANV Allied Nevada Gold 35%

RBY Rubicon Mineral Corp 21%

How is this strong insider interest line up playing out over the past year ? Well, if you take the top 10, leaving off the low 11% of Midway, a lot of which is recent buying; and figure this portfolio's performance, you get +65% vs about +19% for the HUI gold stock index since this time last year.

The problem with gold stocks is you can't depend on our trusty valuation ratios, cash flow curves, or other normally useful parameters. Gold stock value is not about money put on past statements, its all about pulling future ore from their properties. You have to analyze the price of gold with all its complexity and danger. But most importantly, you must look inside the minds of the people who run the companies.

Saturday, September 4, 2010

Are Smartphones A New Recession Play ?

By past investment norms, you wouldn't think an expensive electronic gadget would be considered a secular growth investment to fall back on in a weak economic time. But expensive electronic gadgets have insidiously wound their way into the fabric of our daily lives since past recessions. The coup de grace to the old view of gadgets has to be the smartphone. We have come to depend on these just like our bar of soap in the shower. Companies like Apple have become the new Procter and Gambles, only faster growing.

Along with this changing view of secular growth, Wall Street is coming to the morning after realization that delevering down from the debt binge is going to be a chronic condition afflicting the investing world for some time to come. "Derivatives" used to be thought of as a good and sophisticated thing. Now, when CNBC's in-house rock band thinks up a name for themselves, they come up with "The Derivatives". It reminds me of that episode of the old Dick Van Dyke Show from the mid '60s, when bands first started naming themselves after the most unsettling, disgusting thing they could think of. Rob was second guessing the naming of a band, wondering why they hadn't called themselves "The Festering Sores".

Derivatives and their aftermath are going to be a festering sore for us for a long time to come, unfortunately. So whatever the good secular growth investments are, that's what we want. Smartphones and gold are two that come to mind among defensive, but fast growers. CBS news.com ran a smartphone article last week calling them "seemingly recession proof" and running into the problem of not being able to get enough chips from a chip industry underestimating Jim Cramer's "smartphone tsunami". Cramer seems to be right about what he said well over a year ago - that everyone was underestimating it. He felt so strongly about it that he made up a whole separate stock market, a smartphone index, on August 11, 2009 to show off it's market beating performance. I thought it was a neat idea, because I agreed with him that the market was underestimating it. But upon perusing through the tech stocks, I found some that I felt should be in any such index that he didn't include. So I jotted down a list and called it the "supplemental" index.

So is this index beating the market over a year later? Well, let's see. If you had invested $10,000 in each name, here's how they would have done (as of Sept 2):

Original Index

+ 5694.68 STAR (merged)

- 5777.46 PALM (merged)

+ 1228.08 CIEN

+ 2096.77 TLAB

+ 3956.40 ADCT (merged)

- 3148.23 TKLC

- 2230.68 CTV

- 1211.65 QCOM

+ 2255.40 BRCM

+ 2849.55 NETL

+ 1784.10 XLNX

+ 5247.34 SWKS

+ 833.32 RFMD

- 1200.00 ONNN

+ 1057.65 CY

- 3725.90 TSRA

+11487.36 SNDK

- 377.36 CSCO

+ 176.24 GOOG

- 3869.73 RIMM

+ 5394.40 AAPL

_________

+22520.28 on $210,000 +10.7% vs +8.6% f0r S&P 500

My Supplemental Index

+ 1481.48 WRLS

- 769.20 NTE

+18003.60 ARMH

- 20.00 CHA

- 370.37 SYNA

+ 357.15 CHU

+ 1842.87 LLTC

+ 7459.27 OVTI

+ 16367.93 AKAM

+ 5999.64 CREE

- 2000.00 ERTS

- 833.30 STX

__________

+47519.07 on $120,000 +39.6% vs +8.6% for S&P 500

Combining the two lists together, we get +21.2% - a serious outclimbing of the market, but taking a back seat to gold's +31.8% over that period. Let the bad times roll!

Along with this changing view of secular growth, Wall Street is coming to the morning after realization that delevering down from the debt binge is going to be a chronic condition afflicting the investing world for some time to come. "Derivatives" used to be thought of as a good and sophisticated thing. Now, when CNBC's in-house rock band thinks up a name for themselves, they come up with "The Derivatives". It reminds me of that episode of the old Dick Van Dyke Show from the mid '60s, when bands first started naming themselves after the most unsettling, disgusting thing they could think of. Rob was second guessing the naming of a band, wondering why they hadn't called themselves "The Festering Sores".

Derivatives and their aftermath are going to be a festering sore for us for a long time to come, unfortunately. So whatever the good secular growth investments are, that's what we want. Smartphones and gold are two that come to mind among defensive, but fast growers. CBS news.com ran a smartphone article last week calling them "seemingly recession proof" and running into the problem of not being able to get enough chips from a chip industry underestimating Jim Cramer's "smartphone tsunami". Cramer seems to be right about what he said well over a year ago - that everyone was underestimating it. He felt so strongly about it that he made up a whole separate stock market, a smartphone index, on August 11, 2009 to show off it's market beating performance. I thought it was a neat idea, because I agreed with him that the market was underestimating it. But upon perusing through the tech stocks, I found some that I felt should be in any such index that he didn't include. So I jotted down a list and called it the "supplemental" index.

So is this index beating the market over a year later? Well, let's see. If you had invested $10,000 in each name, here's how they would have done (as of Sept 2):

Original Index

+ 5694.68 STAR (merged)

- 5777.46 PALM (merged)

+ 1228.08 CIEN

+ 2096.77 TLAB

+ 3956.40 ADCT (merged)

- 3148.23 TKLC

- 2230.68 CTV

- 1211.65 QCOM

+ 2255.40 BRCM

+ 2849.55 NETL

+ 1784.10 XLNX

+ 5247.34 SWKS

+ 833.32 RFMD

- 1200.00 ONNN

+ 1057.65 CY

- 3725.90 TSRA

+11487.36 SNDK

- 377.36 CSCO

+ 176.24 GOOG

- 3869.73 RIMM

+ 5394.40 AAPL

_________

+22520.28 on $210,000 +10.7% vs +8.6% f0r S&P 500

My Supplemental Index

+ 1481.48 WRLS

- 769.20 NTE

+18003.60 ARMH

- 20.00 CHA

- 370.37 SYNA

+ 357.15 CHU

+ 1842.87 LLTC

+ 7459.27 OVTI

+ 16367.93 AKAM

+ 5999.64 CREE

- 2000.00 ERTS

- 833.30 STX

__________

+47519.07 on $120,000 +39.6% vs +8.6% for S&P 500

Combining the two lists together, we get +21.2% - a serious outclimbing of the market, but taking a back seat to gold's +31.8% over that period. Let the bad times roll!

Wednesday, September 1, 2010

Simulations Plus Is Worth Watching

There aren't many stocks outside the gold universe that reside on my "A" list, but this is one of them. Stocks in general seem to be in a condition where they get jerked around by the latest fret or relief rally over global finances. Finding those that are dancing to their own music these days is tough. Simulations Plus (SLP) is a tiny company that seems to be doing just that. They in a good area of the market, "para-pharma". They assist drug companies with research programs, so they aren't that economy dependent. And the healthcare overhaul uncertainty storm has blown over. It's technical condition presents a plethoria of positives:

In addition to a nice looking cup and handle bottom, long since completed, it has been working on a resistance level at around $2. Earlier this year, this resistance was broken then successfully tested as support. This seems to be one of those stocks that likes to sneak up on investors and clobber them with a big climb after they've left the building. The chart shows the big moves up only after volume has gotten very quiet. It is at such a stage right now. It's trading close to a parallel 140/200 ema that has established a smooth uptrend. The stock was totally oblivious to the nasty tumble in February and the dive after April.

Fundamentally, eps has been in a steady climb since '05 with only a mild interruption in '09 (up over 100% in 5 years), and the ttm eps is up from '07 while the stock has been smashed from $8 to less than $2. Debt is zero, current ratio over 9, and the insiders love it, carrying a whopping 47% of the shares.

It's no gold stock, and it's not smartphone, but maybe the next best thing.

In addition to a nice looking cup and handle bottom, long since completed, it has been working on a resistance level at around $2. Earlier this year, this resistance was broken then successfully tested as support. This seems to be one of those stocks that likes to sneak up on investors and clobber them with a big climb after they've left the building. The chart shows the big moves up only after volume has gotten very quiet. It is at such a stage right now. It's trading close to a parallel 140/200 ema that has established a smooth uptrend. The stock was totally oblivious to the nasty tumble in February and the dive after April.

Fundamentally, eps has been in a steady climb since '05 with only a mild interruption in '09 (up over 100% in 5 years), and the ttm eps is up from '07 while the stock has been smashed from $8 to less than $2. Debt is zero, current ratio over 9, and the insiders love it, carrying a whopping 47% of the shares.

It's no gold stock, and it's not smartphone, but maybe the next best thing.

Sunday, August 15, 2010

Another Iran Worry

This week, we investors must pass through another one of those heightened geopolitical risk windows over the Iran/Israel stand-off. I've posted on some of these. Russian is delivering the fuel to operate the Bushehr nuclear plant August 21. Speculation is that an Israeli strike will be done before the plants are filled with the fuel that will make a radioactive mess if bombed. This may kill millions in heavily populated neighbor regions. Israel hit the other two nuclear plant threats, the Iraqi plant in '81 and the Syrian plant in '07, before they were supplied with fuel. So we are in a danger zone. Late 2009 was such a zone when the Obama initiated enrichment offer was put together - then rejected by Iran. Israel now seems to be waiting, perhaps on the MOP bunker busters from Boeing, said last year to be ready by July, 2010. Or perhaps they are waiting on American efforts at disrupting Iran from within. There is a large article out this weekend in The Atlantic titled The Point of No Return. The informed opinion presented here leans toward more forbearance (more waiting) by Israel over the coming months.

You would think, as John Bolton does, that Isarel is constrained to make their military move before any plant fueling. But the radiation mess is just one of many messes being weighed into the calculus. So we may not be very well served with this week's fueling schedule as a military schedule.

Regardless of when the strike happens, the conscientious investor has to try to anticipate the market implications. You could stay totally out of all markets until a military option is taken. That would have kept you out of the Cold War market from 1957 to 1989. Or you can study what past Middle East blow ups did, and weight portfolios accordingly. If you look at the two most recent Middle East blow ups, Saddam's invasion of Kuwait in August of 1990 and Bush's announcement that we were going to invade Iraq, believed to be chock full of bio and chemical weapons in late 2002, you see that the two beneficiaries are oil and gold. In the 1990 blow up: (click to enlarge charts)

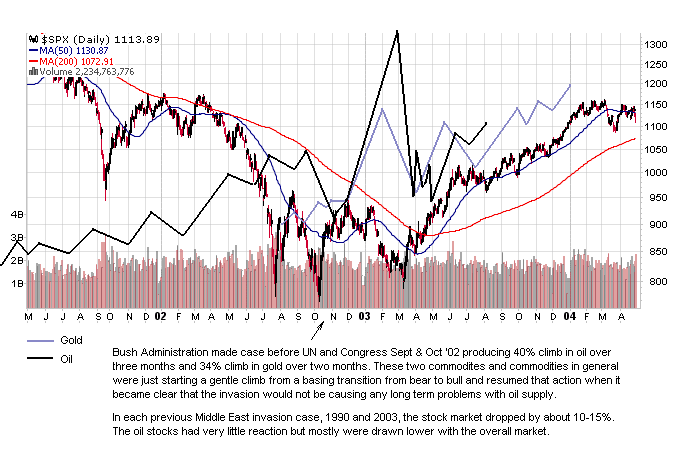

And in the 2002 blow up:

These two time frames were during a bear market in commodities (1990) and a beginning bull market (2002). The geopolitical events caused just a brief detour by gold and oil from the paths they were taking, demonstrating the power of macro-economic trends over geopolitical events. Of course Iran/Israel may be a macro-economic trend changer if it were to occur.

It's worth noting that oil stocks didn't do much over these past shocks, but gold stocks typically did about whatever gold did. So of the four good "shock" investments that come to mind - gold, oil, gold stocks, and oil stocks - we've had 3 up and one down over past shocks.

But, based on my conversations with Israeli decision-makers, this period of forbearance, in which Netanyahu waits to see if the West’s nonmilitary methods can stop Iran, will come to an end this December. Robert Gates, the American defense secretary, said in June at a meeting of NATO defense ministers that most intelligence estimates predict that Iran is one to three years away from building a nuclear weapon. “In Israel, we heard this as nine months from June—in other words, March of 2011,” one Israeli policy maker told me. “If we assume that nothing changes in these estimates, this means that we will have to begin thinking about our next step beginning at the turn of the year.”

You would think, as John Bolton does, that Isarel is constrained to make their military move before any plant fueling. But the radiation mess is just one of many messes being weighed into the calculus. So we may not be very well served with this week's fueling schedule as a military schedule.

What is more likely, then, is that one day next spring, the Israeli national-security adviser, Uzi Arad, and the Israeli defense minister, Ehud Barak, will simultaneously telephone their counterparts at the White House and the Pentagon, to inform them that their prime minister, Benjamin Netanyahu, has just ordered roughly one hundred F-15Es, F-16Is, F-16Cs, and other aircraft of the Israeli air force to fly east toward Iran—possibly by crossing Saudi Arabia, possibly by threading the border between Syria and Turkey, and possibly by traveling directly through Iraq’s airspace, though it is crowded with American aircraft.

Regardless of when the strike happens, the conscientious investor has to try to anticipate the market implications. You could stay totally out of all markets until a military option is taken. That would have kept you out of the Cold War market from 1957 to 1989. Or you can study what past Middle East blow ups did, and weight portfolios accordingly. If you look at the two most recent Middle East blow ups, Saddam's invasion of Kuwait in August of 1990 and Bush's announcement that we were going to invade Iraq, believed to be chock full of bio and chemical weapons in late 2002, you see that the two beneficiaries are oil and gold. In the 1990 blow up: (click to enlarge charts)

And in the 2002 blow up:

These two time frames were during a bear market in commodities (1990) and a beginning bull market (2002). The geopolitical events caused just a brief detour by gold and oil from the paths they were taking, demonstrating the power of macro-economic trends over geopolitical events. Of course Iran/Israel may be a macro-economic trend changer if it were to occur.

It's worth noting that oil stocks didn't do much over these past shocks, but gold stocks typically did about whatever gold did. So of the four good "shock" investments that come to mind - gold, oil, gold stocks, and oil stocks - we've had 3 up and one down over past shocks.

Subscribe to:

Posts (Atom)